Can You Squeeze Water from a Stone?

Ethiopia's Banks Face a Deposit Dilemma

The adage is simple: you can't extract something from nothing. Yet, a disquieting trend is emerging within Ethiopia's private banking sector, suggesting an attempt to defy this fundamental truth. This blog was inspired by a recent exposé by Meseret Media, which offered an in-depth look at the psychological burden employees at private banks are enduring. This distress is a direct result of unmet and increasingly unrealistic demands from upper management, forcing employees to secure a significant number of new customer accounts within impossibly short deadlines.

I extend my gratitude to the columnist for bravely delving into such a pressing issue that, as the report suggests, is transforming the workplace into a "hell of fire." This investigative journalism has done a great service by allowing overstressed employees to voice their outcry and agony—a situation for which no immediate, humane solution seems to be at hand.

Economic Headwinds and Eroding Savings

The backdrop to this aggressive deposit drive is a challenging macroeconomic reality. Ethiopia's inflation rate stood at 19.9% in June 2024, a significant decrease from 29.3% during the same period last year. Despite this improvement, the high inflation continues to erode purchasing power, leaving the average Ethiopian with diminished capacity for personal savings. What little disposable income existed is now stretched thin, struggling to cover the increasing costs of basic necessities. For many, life has truly become a "hand-to-mouth" existence.

Adding to this pressure is the government's fiscal stance. In a bid to manage its budget deficit without resorting to printing money (directly borrowing from National Bank of Ethiopia)—a commitment made to the IMF—we've witnessed a rise in fuel prices, property tax and utility tariffs, amongst other costs. These measures, while aimed at fostering macroeconomic stability, have further tightened the financial belts of the general public, leaving meager resources for savings.

Unrealistic Burdens, Unsustainable Strategies

Against this stark economic landscape, the directive for bank employees, including drivers, to bring in millions in deposits seems not just ambitious, but utterly detached from reality. Are we to believe that drivers, navigating the bustling streets of Addis Ababa, possess a hidden network of individuals flush with cash, just waiting to open high-value accounts? The pressure placed on these employees breeds stress and demoralization for a task that seems inherently impossible given the economic constraints faced by the majority of the population.

It appears that the previous emphasis on branch expansion has led banks to hire an excess workforce. Undeniably, the ever-rising cost of living has compelled banks to implement salary raises and adjustments year-on-year to keep pace with exorbitant expenses. From a business perspective, banks cannot sustain bloated expenses while failing to mobilize enough deposits to lend to businesses and earn profit.

This brings forth two fundamental questions. First, why would a customer be willing to deposit millions of Birrs to earn a mere 7% interest income when inflation so heavily erodes its value? Large depositors are often motivated by the prospect of securing loans from the bank in return for their deposits. However, the decision to grant a loan is not within the control of the frontline bankers, who are deeply involved in the difficult task of convincing customers simply to open an account.

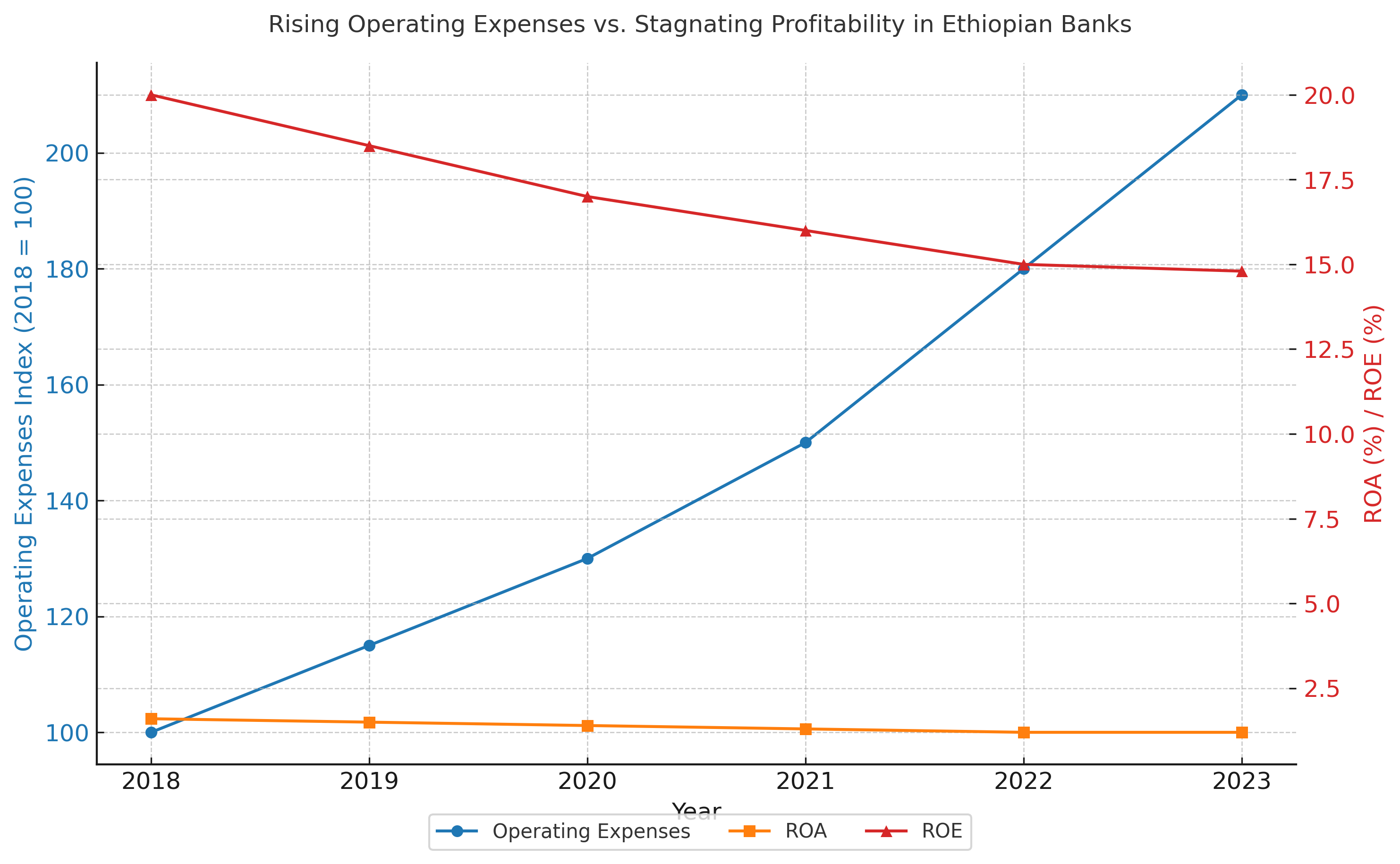

Second, the soaring expenses borne by banks, which are clearly not commensurate with their increase in income, are unsustainable, making cost-cutting measures inevitable. In light of this, putting undue pressure on employees under the guise of deposit mobilization risks paving the way for them to resign without proper compensation. Such a move is unacceptable by any standard. If banks are considering layoffs, the rule of law must be respected, and employees need to be compensated transparently as required by law. The below figure that depicts the ever rising in expenses accompanied by stagnating profitability is taken from the financial stability report of National Bank of Ethiopia.

Digital Banking: From Pressure to Progress

Ethiopia’s banking sector must abandon outdated, coercive deposit mobilization tactics and embrace a digital-first strategy rooted in inclusion and innovation. As platforms like Telebirr demonstrate—with over 50 million users and a vast agent network—customers value speed, accessibility, and simplicity. Banks should digitize onboarding, expand mobile and agent banking, and develop digital savings tools. Instead of unrealistic targets, banks should analyze behavioral data to tailor messaging, send nudges, offer loyalty rewards, and optimize customer retention strategies. Kenya offers a powerful lesson: after M-Pesa’s disruption, its banks adapted by investing in digital channels, resulting in over 80% of adults using mobile financial services today. Ethiopia can chart a similar path if banks modernize operations and the National Bank of Ethiopia sets clear goals—such as requiring 50% of deposits to come via digital channels by 2026.

Great insights that inform the banking sector to think strategically, and realistically in a pragmatic way